How to Finance a Roof: What Homeowners Need to Know

Oct 13, 2025At a Glance: Most homeowners can finance a new roof through home equity loans, personal loans, credit cards, or insurance claims. The best option depends on your credit score, home equity, and whether the roof damage is covered by insurance. When selecting your financing path, focus on the total cost including interest, whether the monthly payments fit your budget, and if the funding timeline aligns with your roofing project schedule.

A new roof is one of the biggest investments you’ll make in your home, typically costing between $10,000 and $50,000. While roofing expenses can feel overwhelming, there are several financing paths that can make roof replacement more manageable for your budget. Many homeowners don’t realize they have multiple options beyond paying cash, from tapping into home equity to working with insurance companies. Understanding your roof financing choices, from traditional bank loans to insurance claims, helps you make smart decisions about protecting your home without straining your finances.

Understanding Your Financing Options

Home equity loans and home equity lines of credit (HELOCs) are the most popular choices for financing a new roof, but there are several options that homeowners can explore.

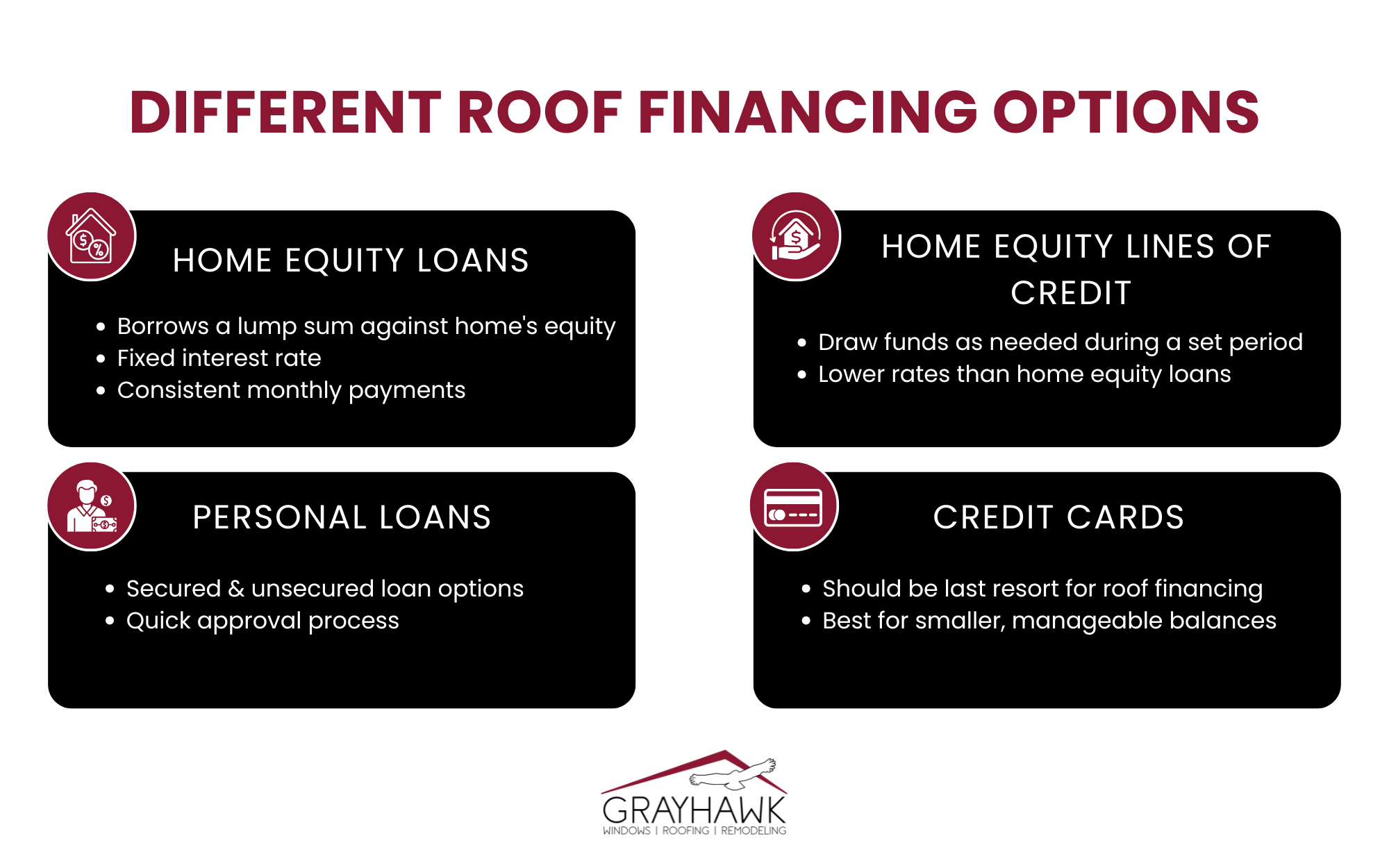

Home Equity Loans

With a home equity loan, you borrow a lump sum against your home’s equity, typically receiving a fixed interest rate and consistent monthly payments. To qualify, you’ll need:

- At least 15-20% equity in your home

- Credit score of 620 or higher

- Debt-to-income ratio below 43%

Current home equity loan rates average between 6-8%, but these can fluctuate depending on the lender and credit score. Repayment terms typically range from 5 to 30 years.

Home Equity Lines of Credit (HELOC)

HELOCs function like a credit card secured by your home. You can draw money as needed during a set period, usually making interest-only payments initially. While HELOCs often start with lower rates than home equity loans, these rates are variable and may increase over time. Some banks may offer initial fixed-rate periods.

Personal Loans

The application process for a personal loan is straightforward: lenders review your credit score, income, and debt levels. Most personal loans offer terms between 2-7 years.

Secured Personal Loans

- Use collateral to protect the lender

- Lower interest rates (typically 4-12% based on credit score)

- Asset loss risk if the loanee defaults

Unsecured Personal Loans

- Don’t require collateral

- Higher interest rates (typically 8-36% based on credit score)

Credit Cards

Credit cards should generally be your last financing choice for a new roof. However, they can make sense if you qualify for a card offering 0% APR on purchases for 12-18 months. Some home improvement stores partner with credit card companies to offer special financing deals.

The main advantage is immediate access to funds, but standard credit card interest rates often exceed 20% once promotional periods end. Consider this option only if you can pay off the balance before higher rates kick in.

Insurance and Assistance Programs

Insurance claims and government programs can help finance your new roof when you’re facing significant costs.

Homeowners Insurance

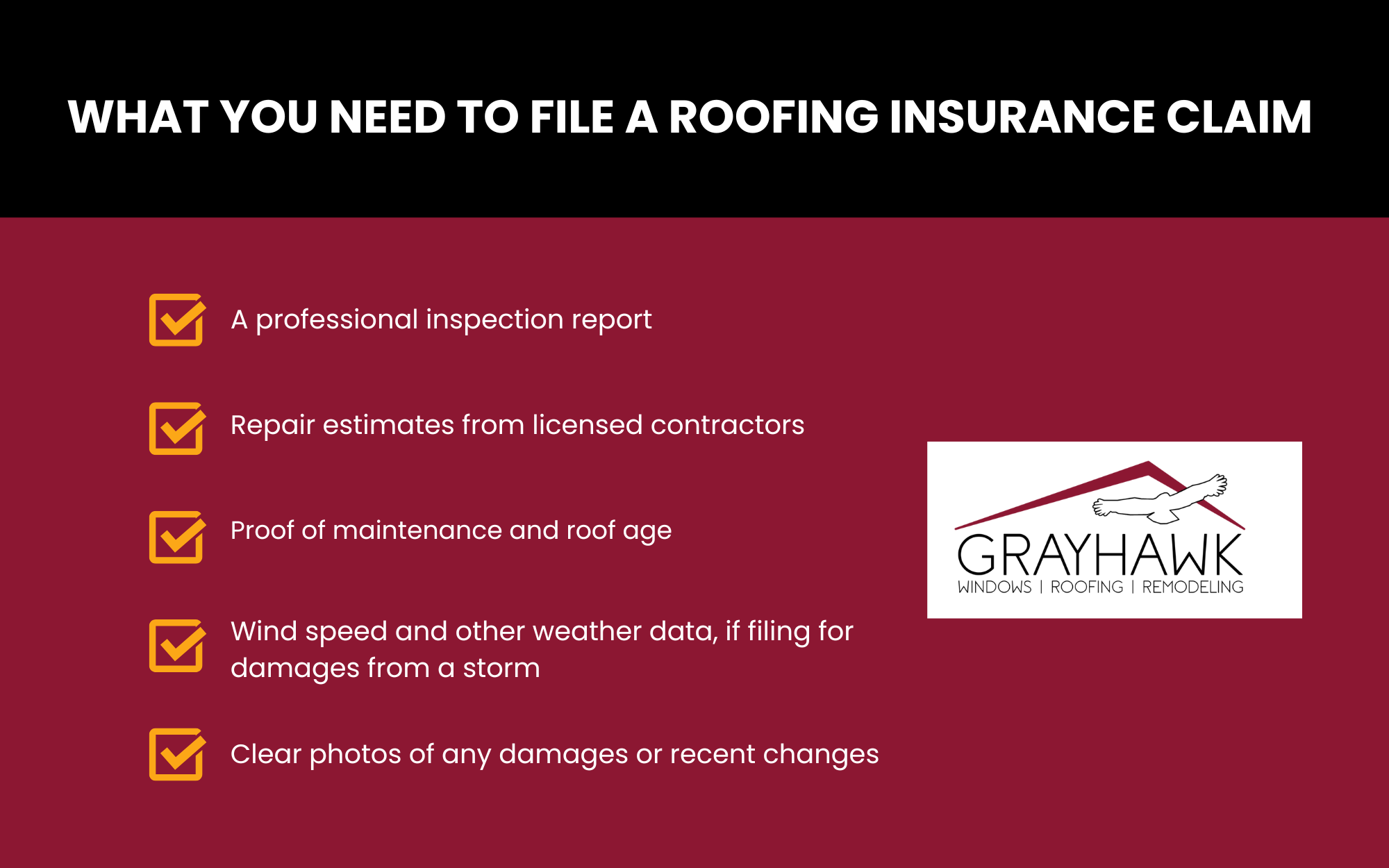

These plans often cover roof replacement when damage occurs from specific events like storms. To file a claim, you’ll need:

- A professional inspection report

- Repair estimates from licensed contractors

- Proof of maintenance and roof age

- Wind speed/weather data from the storm

If you notice damage on your roof, contact your insurance company immediately. They’ll send an adjuster to inspect your roof and determine what insurance coverage you’re eligible for.

Documentation

When working with an insurance company, document everything thoroughly:

- Take clear photos of the damage

- Save receipts for temporary repairs

- Keep records of all communication with your insurance company

The typical claims process takes 2-4 weeks, though hurricane damage claims may take longer during peak storm seasons.

Title I Programs

The Department of Housing and Urban Development (HUD)’s Title I Home Loan Program offers loans up to $25,000 for home improvements, including roof replacement. These loans don’t require home equity and feature lower interest rates than many credit cards or personal loans. To qualify, you’ll need:

- A debt-to-income ratio under 45%

- Steady employment history

- Clean credit report

- Property as your primary residence

Federal, State, & Local Options

Some homeowners have additional state, city, and county-based local options for roof financing.

- Low-Income Programs: The U.S. Department of Agriculture’s Rural Development division provides loans to very-low-income homeowners to repair, improve or modernize their homes through their Single Family Housing Repair Loans & Grants.

- Senior Programs: Elderly very-low-income homeowners can access grants to remove health and safety hazards through the Single Family Housing Repair Loans & Grants. The HUD also offers Home Equity Conversion Mortgages for seniors.

- Storm-Prone Areas: Places with frequent destructive weather often have special funding after hurricanes and major storms. For example, the My Safe Florida Home program provides matching grants up to $10,000 for hurricane-hardening improvements.

Most insurance companies require claims submission within one year of the damage date, but filing quickly improves your chances of approval.

Contractor Payment Plans and Financing

Many roofing contractors, including Grayhawk Remodeling, offer in-house financing options to help homeowners manage the cost of a new roof. Working directly with your contractor can simplify the payment process and potentially save you money through special promotions or partnerships.

Direct Financing Through Contractors

Many roofing companies partner with finance companies to offer short and long-term payment plans. Monthly payments vary based on your credit score and chosen term length.

- Short-Term Financing: Typically range from 6 to 18 months

- Longer-Term Financing: Can last from 18 months up to 10 years

Roofing Company Partnerships

Contractors frequently work with established lending partners like Synchrony, GreenSky, or Wells Fargo Home Projects. Standard payment terms can include fixed monthly payments, no prepayment penalties, zero-down options, and the ability to finance the entire project, including materials and labor.

Grayhawk Remodeling works with trusted financial partners Buildertrend, Service Finance, and RENEW Financial’s P.A.C.E program to provide flexible payment options that fit the various budgets and timelines of Florida homeowners.

What to Look for in Roofing Contractor Financing

When comparing contractor financing offers, focus on:

- Total interest paid over the loan term

- Length of any 0% promotional period

- Monthly payment amount

- Prepayment penalties or fees

- Contractor’s relationship with the lender

Watch out for extremely high interest rates after promotional periods end, pressure to sign immediately, or contractors who seem unclear about their financing terms. Many contractors can adjust terms or match competitors’ offers to earn your business, so don’t hesitate to negotiate.

Find a Financing Solution for Your Roof with Grayhawk Remodeling

Thanks to the range of options available today, financing a new roof doesn’t have to be overwhelming. From home equity loans and personal loans to specialized roofing financing programs, homeowners can find a solution that matches their financial situation and timeline needs. Compare interest rates and terms across multiple lenders, and read all documentation carefully before signing. Remember that putting some money down initially can often secure better rates and lower your monthly payments.

Grayhawk Remodeling offers several standard and creative roof financing options in Bradenton and Sarasota counties. Our expert team will walk you through available options and help you choose a plan that works best for your needs. With over 30 years of local experience, Grayhawk is here to make your roofing project as affordable and stress-free as possible.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}